Our operating environment: material trends

The impacts of Covid-19 and the associated lockdown restrictions have significantly increased complexity in our operating context, amplifying the existing challenges of a constrained consumer environment, growing competition, and changing consumer and regulatory expectations. Despite the very challenging business context, consumer packaged goods (CPG) companies in South Africa have performed comparatively well against other sectors, benefiting from being an essential service and from the increase in at-home consumption.

This year we have identified five trends in our operating environment that have a material impact on Tiger Brands’ ability to create value. Each of these trends presents both risks and opportunities that continually informed the development of our growth strategy

Tiger Brands depends on a strong economy and healthy consumer demand to drive sales of its premium branded products.

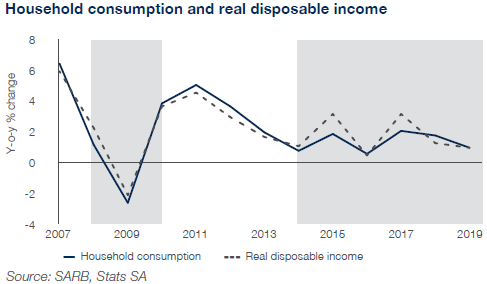

The South African economy remains weak, with a volatile exchange rate and the majority of households under significant financial pressure. Pre-Covid-19, the economy contracted by 1,4% in the fourth quarter of 2019, following a contraction of 0,8% in the third quarter. This technical recession was profoundly impacted by the national lockdown introduced at the end of March 2020, with the economy slipping into a recession much faster and deeper than expected. Consumer confidence has dropped to its lowest level since 1985, with heightened job losses further denting consumer spend, reducing demand for discretionary and premium products, and increasing demand for “value” offerings. Volumes and margins remain threatened, and cost recovery ahead of inflation becomes difficult.

|

Key features of this trend impacting value creation include:

|

|

- In an effort to protect margins in the subdued market, we have kept a strong focus on driving productivity and securing cost efficiencies across the value chain (see Be efficient).

- During the year, various significant investments were approved aimed at enhancing efficiency and realising innovation opportunities (see Be efficient).

- We placed a strengthened emphasis on boosting economic opportunities and improving the livelihoods of thousands of people across our value chain, including through a deliberate focus on supporting black/black women farmers and owned enterprises (see Sustainable future and sustainability report).

Tiger Brands increasingly depends on its ability to adapt in a maturing market.

Food retail has diversified, with increasing online engagement and digital sales. New producers are establishing strong premium brands and successful niche products. While supermarkets remain the leading distribution channel in packaged food, the channel is seeing strong competition from mixed retailers. Retailers have hardened their procurement practices, and in many instances have further increased uptake of private label, which is doing well in shelf stable and dairy products. This has contributed to increased pressure on returns, volumes and market share, intensified price competition, and heightened promotions, inspiring differentiation towards richer value-propositions that undercut margins. These dynamics challenge our historic brand advantage but are inspiring us to become more agile.

Key features of this trend impacting value creation include:

- Heightened competition from brands and private label

- Increased promotional activities

- Innovation in products, process and approach

- Increasing differentiation to enhance value offerings

- Weaker volumes, price competition and margin pressure.

- We seek to mitigate the risks and realise the opportunities associated with the changing retail and consumer dynamics by delivering on our strategic ambition to drive growth. We have identified opportunities to optimise our product portfolio, respond to the growth in private label brands, and win at the point of purchase (see Drive growth).

- We have been implementing channel-specific category management methodologies and will be continuing to embed appropriate digital technologies that enhance the monitoring of the return on investment of our promotional activity, while meeting customers’ needs, and we have been using new pricing expertise to help drive brand growth and customer support.

- We made further progress this year in launching new products to address consumer expectations for quality, convenience, healthier foods and affordable pack sizes. Despite the heighted competition we retained the lead in packaged food, with a 26% value share (see Group profile).

Convenience foods, health and wellness, affordability, and e-commerce heighten need for innovation

Shifting patterns of consumer behaviour are leading to significant changes in the food system, driven by trends such as rapid urbanisation and globalisation, increasing digital connectivity and mobility, and the rising number of single households and at-home consumption. Dietary shifts reflect these changing global patterns and economic aspirations, with growing public health concerns offset by the strong uptake of processed products, convenience foods, and snacks and beverages. With more meals now consumed at home, consumers are looking for inspiration for home cooking and baking. On the surface is the everyday impact of deepening economic pressure on households; not only are consumers buying and spending less, but shopping smarter and more ethically, seeking not only greater value-for-money, but greater value-for-all.

Key features of this trend impacting value creation include:

- A dramatic rise in e-commerce following the Covid-19 lockdown restrictions

- More meals consumed at home

- Health and wellness trend gain momentum across packaged food

- Increasing price consciousness and decreasing brand loyalty

- Increasing demand for “more value”

- Improving perception of private labels.

- We continually review consumer trends to identify opportunities for product and process innovation and to optimise our product portfolio. We have an exciting product pipeline across a range of categories that specifically include innovations for value-seeking consumers, supported by a robust marketing and communication plan highlighting the benefits and relevance of our current brands within the value segment.

- Covid-19 has accelerated the adoption of e-commerce behaviour amongst consumers, with South African food retailers reporting a 700% increase in web traffic volumes. In addition, there is evidence that there is a 70% likelihood of consumers continuing to buy groceries online. In response to this trend, Tiger Brands has listed on major e-tailing and retailers’ online platforms.

- We believe that there are valuable opportunities in the health and nutrition sector, and have been driving innovation in this area including launching new healthy product lines in the Baby and Personal Care categories, introducing consumer-relevant health claims in various brands, and beginning the process of including portion control messaging on the back of packs in the Snacks & Treats category.

- Through the diversity of our portfolio we are able to address the full range of consumers’ shopping needs, particularly those in the middle-income bracket.

Tiger Brands recognises the importance of building an ethical and sustainable business practice.

South Africa’s food system is one of the least healthy globally, characterised by high levels of obesity, lifestyle-induced non-communicable disease (NCD) and persistent hunger and malnutrition. Increasing consumer and investor activism on environmental, social and governance (ESG) issues, and emerging regulatory interventions, reflect a growing concern to address the negative nutritional, health and environmental outcomes of the food system, placing greater pressure for industry action, transparency and accountability. The Sustainable Development Goals (SDGs) provide a benchmark for clear targets and an increasing number of global industry initiatives demand collective action. Enhanced regulatory and voluntary interventions have introduced new marketing, health and environment-related control mechanisms, regulations and taxes. An increased possibility of litigation threatens resources and reputation. Higher income consumers are more willing to trade-off on price for health and sustainability, with increasing demand for brands-with-purpose, sustainable and local products, plant-based proteins, ethical marketing and front-of-pack nutrition labels. These shifts challenge some traditional business approaches and encourage the adoption of purpose-led innovation.

Key features of this trend impacting value creation include:

- Pressure to align with global agreements and voluntary initiatives

- Pressure to address environmental concerns such as climate change, water, plastics and sustainable agriculture

- Pressure to promote social transformation on issues such as race, gender and income inequality, and land rights

- Increasing regulatory intervention on public health, obesity and NCDs

- Growing demand for purpose-led brands and products.

- In delivering on our purpose, we have made important progress this year on our commitment to enabling consumers to improve their health and wellbeing. We have updated our nutritional standards against global guidelines, introduced a three-tier product offering approach informed by these guidelines, and made progress in establishing a baseline and setting targets for more nutritious products as a percentage of our total portfolio (see Sustainable future and sustainability report).

- We have continued to invest significantly in driving quality and food safety across the company to ensure that we have robust management systems, qualified people, and a strong quality culture. We have strengthened our audit and assessment processes, achieving external certification for all our manufacturing facilities against globally recognised food safety standards, and starting the certification process for our warehouses (see Sustainable future and sustainability report).

- We are striving to reduce our environmental impact through innovative solutions, including optimising energy and water usage, developing innovative products and packaging, leveraging our brand and marketing, and implementing circular economy initiatives that stimulate economic opportunities (see Sustainable future and sustainability report).

Covid-19 and the associated economic shutdown has deepened some of the existing trends, negatively impacting consumer spend, further driving the uptake of e-commerce and at-home consumption, and heightening consumer concerns on health and wellbeing. Spending patterns have shifted to staples and essentials, with consumer choice shaped primarily by price, value and convenience. Regulations that capped gross and operating margins on essential products, prohibited price increases and further challenged cost recovery. Direct costs to business included elevated distribution costs and stock challenges, supply chain disruptions, and the purchase of personal protective equipment. There has been an accelerated growth of home consumption and online shopping, and reduced ability to influence choice in-store. The lockdown increased the consumption of digital channels in South Africa by 72%, with continued growth anticipated over the next months. With consumers spending more time online and on social media, advertising has focused increasingly on digital channels. Throughflow at retail outlets was impacted by shorter opening hours, social distancing and customer limitations, prompting consumers to shop less often for bigger baskets. The lockdown restrictions have exacerbated poverty, inequality and public health concerns, juxtaposed by some encouraging examples of a collective humanitarian effort, with consumer and stakeholder activism potentially invigorated by the call to “build back better”. While the future remains particularly uncertain, as a food company and essential service, Tiger Brands is better placed than most to maintain its resilience.

The key focus of our response has been to ensure the availability of our products, ensure employee safety and wellbeing, and increase our community food support for those in need (further details are provided in our online sustainability report):

- Following the Declaration of a state of National Disaster, we took various steps to ensure a continuous supply of product in response to initial panic buying, developed and implemented response protocols to ensure product safety, worked with suppliers, logistics and customers to limit disruptions, and provided effective communication to address consumer concerns around food security

- To protect employee safety and wellbeing, we prioritised remote working where possible, introduced health screening and testing for staff at essential services sites accompanied by rigorous hygiene and sanitisation protocols, and provided additional access to wellness support services along with various other measures

- We expanded our existing community food and nutrition programmes for families and school children and extended these to provide for frontline healthcare workers and hospitals, with numerous new initiatives funded by the voluntary forfeiture of a portion of senior leadership salaries and fees.

To realise growth opportunities in a “new normal”, we are implementing measures to capitalise on the recent uptake of e-commerce and home cooking, the changes in in-store shopping dynamics, and the heightened levels of price consciousness and personal health and wellbeing (see Drive growth).